2011 is off to the fastest start from a transaction perspective since this activity has been tracked. The consolidations of solar project portfolios and sales of solar projects continue to dominate the transaction landscape. However, the increased availability of credit has generated a significant increase in private investment both through the acquisition of projects as well as companies within the supply chain.

Q1 2011 Solar Deal Volume Comparison

Contributed by Jack Calderon and Chaim Lubin | Lincoln International

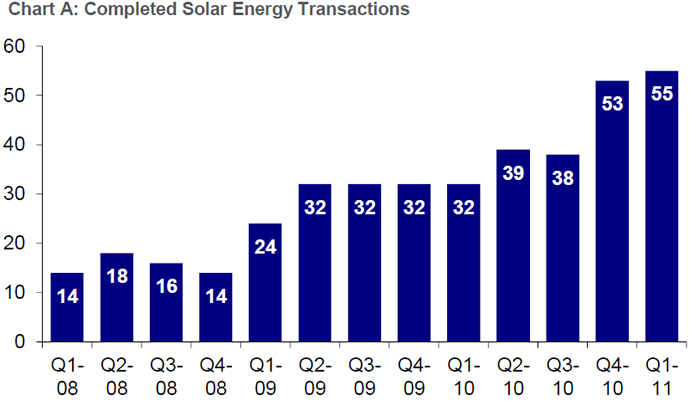

There were 55 completed solar energy transactions in Q1 2011, the greatest number recorded since Lincoln began tracking M&A activity within solar energy. Driving the continued increase in transaction activity are acquisitions of solar projects, consolidations across the supply chain and an uptick in private investment.

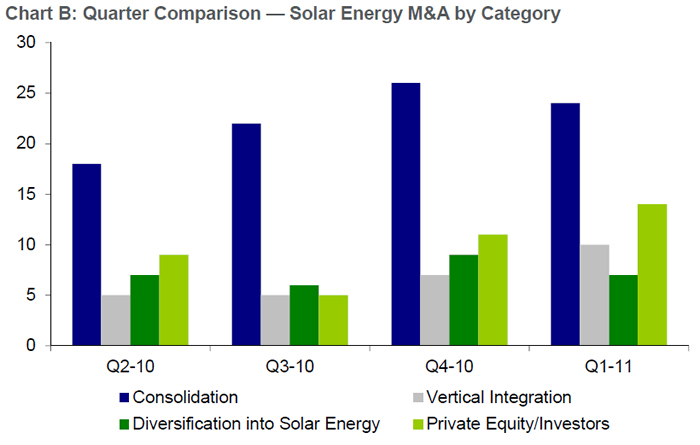

Within the solar energy transactions, consolidation represented 44% of transactions, or 24 deals in Q1 2011. The next largest category was private equity/ investors with 14 transactions, or 25% of the Q1 2011 total. Vertical integration accounted for 10 transactions in Q1 2011, or 18% of the total while diversification into the solar industry by companies accounted for seven transactions, 13% of the quarterly total.

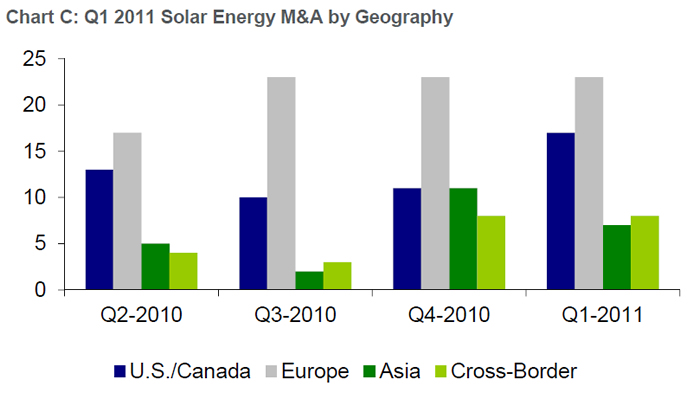

In Q1 2011, 42% of transactions came from Europe, which marks the lowest percentage of total transactions from the geography in over a year. This decline is mainly due to the increased activity from the U.S. and Canada, with 17 transactions, 31% of the Q1 2011 total. Cross-border transactions accounted for eight transactions, or 15% of the total for Q1 2011, while Asia represented seven transactions, 13% of the quarterly total.

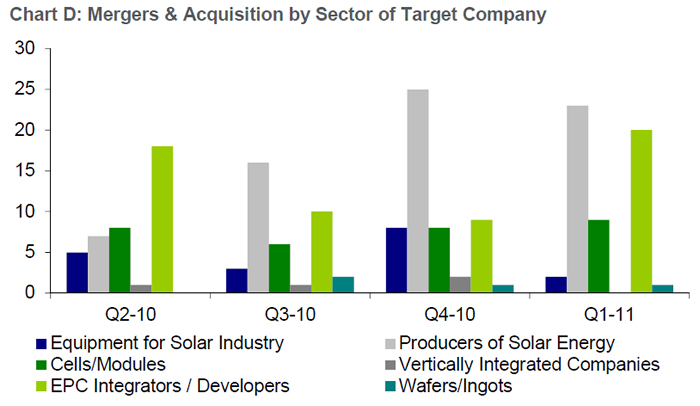

The overriding dynamic that was prevalent again in Q1 2011 but has been occurring steadily over the last few quarters is the large amount of activity amongst companies categorized both as producers of solar energy and amongst EPC integrators / developers. Acquisitions of producers of solar energy accounted for 23 transactions, 42% of the Q1 2011 total. Almost at the same level, there were 20 transactions for EPC integrators / developers, or 36% of the total for Q1 2011. The next largest category was cells / modules producers with nine transactions, or 16% of the total.

There were two transactions of companies categorized as solar equipment providers and one transaction of a company categorized as a wafer / ingot producer, or 4% and 2% of the Q1 2011 total, respectively. Finally, there were no transactions with vertically integrated target companies.

2011 is off to the fastest start from a transaction perspective since this activity has been tracked. The consolidations of solar project portfolios and sales of solar projects continue to dominate the transaction landscape. However, the increased availability of credit has generated a significant increase in private investment both through the acquisition of projects as well as companies within the supply chain. Given the difficulties caused by the re-evaluation of tariff structures across the globe, it is possible that the level of transaction activity could slow over the next quarter, in particular with transactions of solar projects. For now the positive momentum is in full force and companies should evaluate whether there are opportunities to take advantage of the transaction activity to better position themselves in the solar energy industry.

The content & opinions in this article are the author’s and do not necessarily represent the views of AltEnergyMag

Comments (0)

This post does not have any comments. Be the first to leave a comment below.

Featured Product

Terrasmart - Reduce Risk and Accelerate Solar Installations

We push the limits in renewable energy, focusing on innovation to drive progress. Pioneering new solutions and ground-breaking technology, and smarter ways of working to make progress for our clients and the industry.