GlobalData's latest renewable policy report includes major policy developments in the renewable energy market for the month August, 2010. This includes updates in policies in China and the US.

Renewable Policy Analysis - September, 2010

Ms. Gitika Chanchlani | GlobalData

1 China’s Renewable Energy Market Depicts Strong Market Growth

Backed By Government Initiatives

1.1 China’s Clean Energy Policies Backs Its Renewable Energy Market

China’s power market is reliant on its coal reserves. Around 70% of China’s power is produced through

coal-fired power plants. While nuclear energy is one of the alternative options to fossil fuels, China is

shifting its focus towards its renewable power market. In 2006, the country introduced the Renewable

Energy Law to regulate the renewable energy market by providing subsidies, tax incentives, feed-in

tariffs, on-grid power requirements and standard procedures. To support investors, the law also

introduced new financial options as well as cost-sharing mechanisms to share the extra operational costs

among utility customers.

According to the changing market scenarios, the law was further amended to attract the investors to

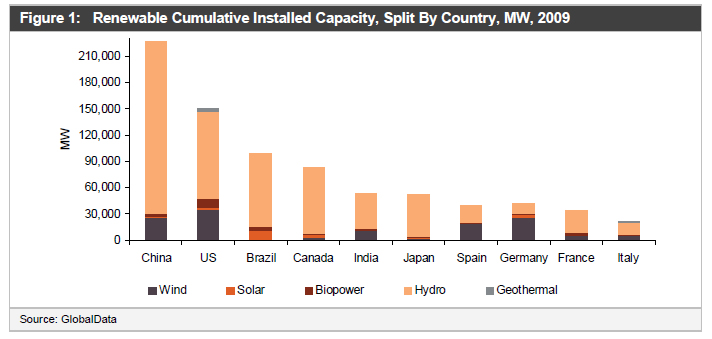

China’s renewable energy market. In 2009, China’s cumulative renewable energy capacity was around

226.5 GW. The US was second to China with its cumulative renewable installed capacity of

approximately 149.8 GW. Hydropower and wind energy sectors accounted for approximately 98.4% of

the total renewable power capacity of China.

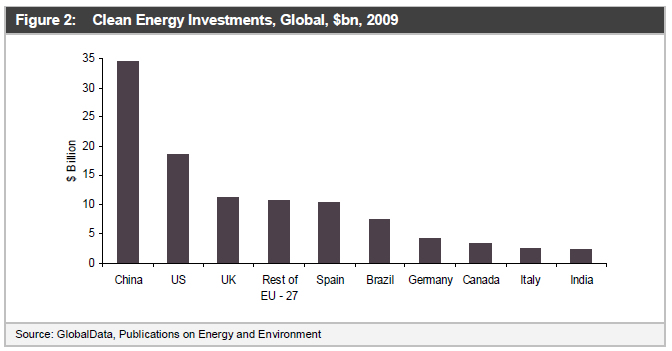

1.2 China Ranked First in the Global Clean Energy Investments in 2009

In 2009, China led investments in clean energy globally, thereby shifting the US to the second position.

With an investment of approximately $34.6 billion in clean energy in 2009, it overtook the US which

invested around $18.6 billion. The mandatory wind and solar power targets together with the easy

availability of project finance are the major drivers for investments in the Chinese clean energy market.

As the country has a strong manufacturing base and large export market, it is now focusing on increasing

its clean energy installed capacity to meet its domestic demand due to increasing renewable energy

targets.

Figure 1: Renewable Cumulative Installed Capacity, Split By Country, MW, 2009

1.2.1 Asset Financing Accounts for 86% of the Clean Energy Investments in China in

2009

Asset financing in global clean energy investments in 2009 decreased by 6% compared to 2008. China

led in global clean energy asset finance investments in 2009, with $29.8 billion of investments. Of the

total clean energy investments in 2009, asset financing accounted for 86% in China.

Public market financing decreased globally as the investor demand slowed down during the financial

crisis. Financing decreased from $22.2 billion in 2007 to $12.1 billion in 2009. However, in this market

scenario, China led the global clean energy public financing market with $4.6 billion investments in 2009.

China’s public financing was driven by strong Initial Public Offering (IPO) activity which occurred in late

2009 to support investments in manufacturing facilities.

1.2.2 Offshore Wind Energy Market Developments

China’s offshore wind energy market is in its nascent stage. It has a minimum of three active offshore

wind projects with a cumulative installed capacity of around 109.5 MW. The Shanghai Donghai Daqiao

102 MW project came online in 2009 operated by the Chinese wind turbine manufacturer, Sinovel.

Around 10 offshore wind power projects are in the planning stage with a cumulative installed capacity of

approximately 3,867.9 MW. In 2009, the National Energy Administration (NEA) focused on the

development of the country’s offshore wind power resources by dividing the potential offshore wind sites

into three categories, which are: inter-tidal zone, offshore zone and deep sea zone. The NEA is expected

to start a concession-tendering process to analyze a tariff range for offshore wind power players. In this

backdrop, China’s wind power capacity is expected to increase due to the exploration of its offshore wind

energy resource potential.

Thus, China’s wind energy market is expected to grow at the same pace. The development of a proper

grid infrastructure, mandatory on-grid connectivity of renewable projects, an increase in the capacity

base of Chinese wind turbine manufacturers to cater to international markets and development of the

country’s offshore wind potential are the major drivers for the growth of China’s wind power market.

These factors are expected to be the cause of the proposal for the revision of the 2020 wind power target

from 30 GW to 150 GW in China.

Figure 2: Clean Energy Investments,

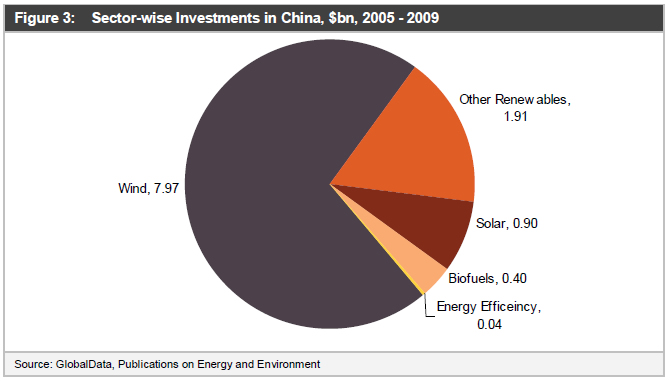

1.2.3 Since 2005, the Highest Investments Have Been in the Wind Energy Sector

Wind energy investments of $7.97 billion accounts for 71% of the total clean energy investments in

2005–2009 in China. Huge investments in the wind energy sector are mainly due to government

initiatives, such as, local content requirement, renewable energy premium, Mandatory Market Share

(MMS) and “Guaranteed Take”. The amendment in Value Added Tax (VAT) rules for wind manufacturing

in 2009 also stimulated the growth of the wind energy sector in the country. By 2009, there were around

80 wind turbine manufacturers in China. Of them, the largest domestic manufacturers, namely Sinovel,

Goldwind and Dongfang have a combined production capacity of 8.2 GW for an annual market of 13.8

GW.

1.3 Outlook

With 9% of the country’s final consumption coming from renewable energy, China is expected to achieve

its 2010 target of generating 10% of the final energy consumption through renewable energy sources. An

increase of approximately 148% in clean energy investments since 2005 depicts the strong growth

potential of China’s clean energy market as the country has been seen as a lucrative option for green

energy investments. Furthermore, government initiatives are also concentrating on increasing the

domestic demand for renewable power in the country. The government is concentrating on the upgrading

of the existing grid infrastructure, which is expected to increase the on-grid power through renewable

energy by connecting remote renewable energy projects to the grid as well as by minimizing

transmission power losses.

Besides China’s fiscal stimulus of around $220 billion, the government plans to invest $738 billion for the

development of its renewable energy sources. Due to its recent support policies in wind and solar

photovoltaic (PV) sectors and strong market growth in 2009, the government has proposed to increase

its wind and solar PV targets by five-fold and 11-fold respectively. Although the government is

concentrating on its clean energy market growth, it should also consider improving its quality standards

to withstand competition by international players.

2 Storage Bill 2010 – Expected Impact in the US Energy Storage

Market

2.1 Storage Bill 2010 – Overview

The Storage Technology of Renewable and Green Energy Bill of 2010 (Storage Bill 2010), revision to the

Storage Act 2009 was introduced in senate on July 20, 2010. The US Senators Jeff Bingaman (D-NM),

Ron Wyden (D-OR), and Jeanne Shaheen (D-NH) introduced the bill for approval. The following are the

various credits that can be availed through the bill.

- The bill allows 20% energy tax credit for investment in energy storage property directly connected to the electrical grid (such as, state systems of generators, transmission lines, and distribution facilities) and designed to receive, store, and convert energy to electricity and deliver such electricity for sale;

- Make such property eligible for new clean renewable energy bond financing;

- Allow 30% energy tax credit for investment in energy storage property used at the site of energy storage; and

- Allow 30% non-business energy property tax credit for the installation of energy storage equipment in a principal residence.

not for companies developing batteries for electric cars. The Storage Bill 2010 would help improve the

efficiency, versatility and reliability of the US electric grid, and would offer more affordable energy storage

technologies for homes and businesses. The proposed law covers three broad categories of storage.

- Commercial Business On-Site Storage

- Residential On-Site Storage

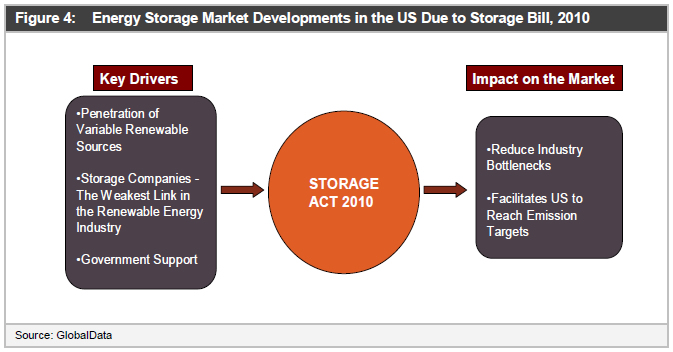

2.2 Energy Storage Market Developments in the US Due to Storage Bill, 2010

The Storage Bill 2010 provides investment tax credits for the actual deployment of storage systems.

Such financial assistance will help reduce energy storage industry bottlenecks as well as encourage the

penetration of energy storage companies in the US renewable energy industry. The following picture

represents the key drivers of the bill and the impact of the bill on the US energy storage market after its

enforcement.

Figure 4: Energy

2.3 Key Drivers of the Bill

The following are the key drivers for the proposal of Energy Storage Bill, 2010:

- Penetration of variable renewable sources

- Storage companies – The weakest link in the renewable energy industry

- Government support

2.4 Impact of the Law

2.4.1 Reduce Industry Bottlenecks

Due to various bottlenecks, it is difficult for the storage companies to penetrate much in the US clean

energy market. High upfront costs, the array of services it provides and the challenges it has in

quantifying the value of these services – particularly the operational benefits such as ancillary services

have been the major barriers for the development of energy storage market in the US. The challenge of

simulating energy storage in the grid, estimating its total value, and actually recovering those value

streams continues to be a major barrier.

2.4.2 Facilitates US to Reach Emission Targets

The enactment of the law will help the country to reduce the dependence on electricity generated from

fossil fuels as well as electricity generated by high carbon-emitting electrical generating facilities to meet

peak load requirements on days with high electricity demand periods. This will also have substantial

benefits from reduced emissions of criteria pollutants. Moreover, the bill is expected to reduce costs to

ratepayers by avoiding or deferring the need for new fossil fuel-powered peaking power plants and

avoiding or deferring distribution and transmission system upgrades and expansion of the grid.

Comments (0)

This post does not have any comments. Be the first to leave a comment below.